Canada Is A Zero

A Record Setting Housing Bubble Bursts, No Room to Stimulate, And a Political Revolt

Email: decodingpolitics@protonmail.com

Substack: decodingpolitics.substack.com

Medium: medium.com/@decodingpolitics

Twitter: twitter.com/DecodingPoliti2

*Not financial advice, merely pointing out political trends*

We have been meaning to write this piece for a long time. Every time we started…..we would get stunned by the enormity of it all. We would track down stats, and more stats. Trying to put it all together would become an overwhelming task. Then we’d move on to something else.

But now we’ve decided we have to publish an introductory piece so people can understand the coming crash across the northern border. Expect more to come over the coming months.

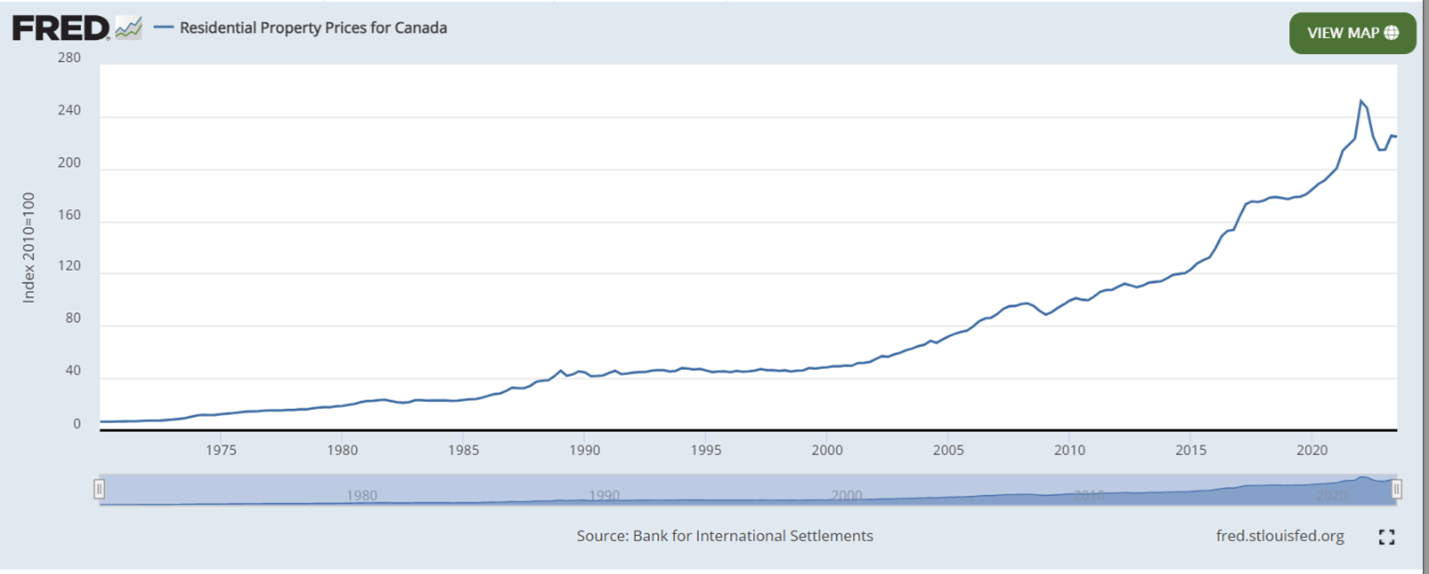

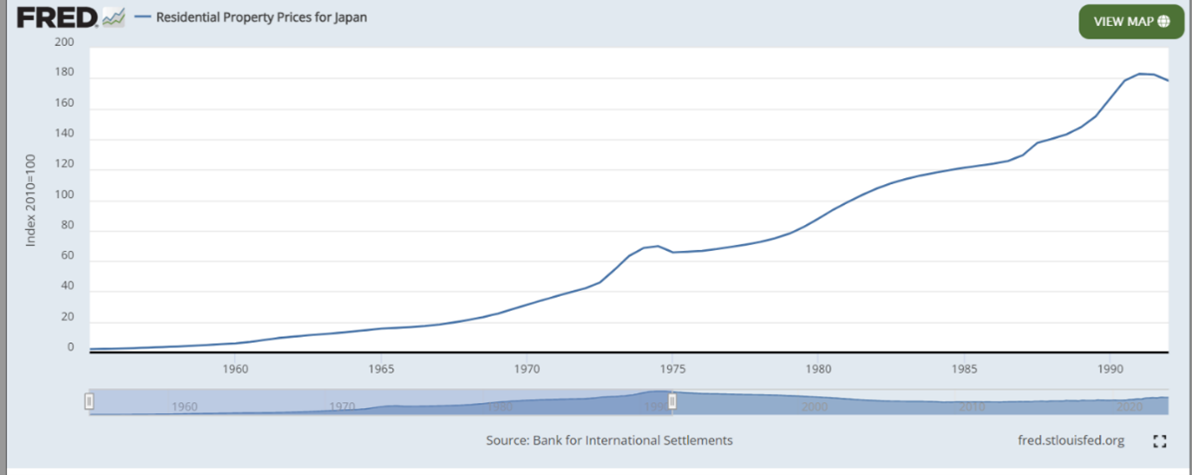

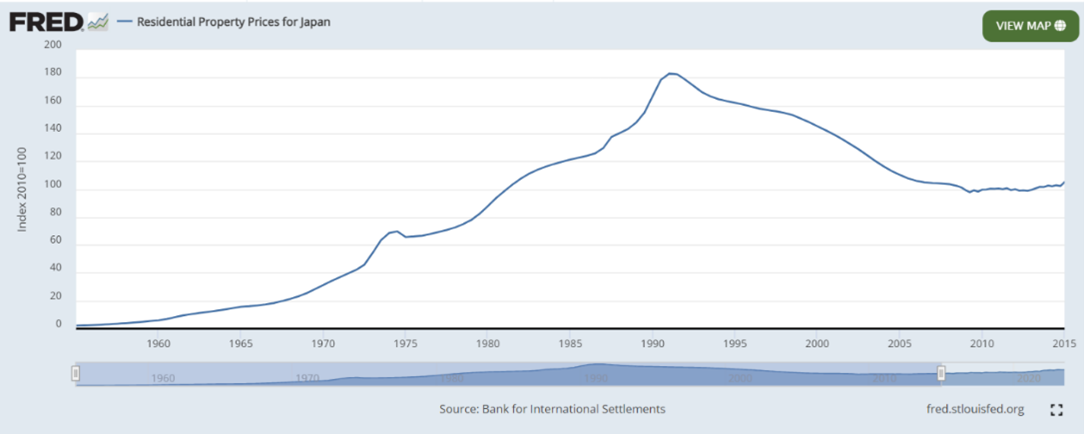

Canada may have the world’s largest real estate bubble of the past forty years. Only Japan in the 1980’s can really compare to the duration, breadth, and magnitude of the insanity of the Canadian property market.

Thanks to its complete unaffordability to regular Canadians, and the massive increase in interest rates since 2021, it seems to have finally begun to roll over. But many are speculating that it will all be fixed once the Bank of Canada start cutting rates again. Or that sustained high immigration, coupled with low housing starts, means that it will put upward pressure on prices.

Sorry to report that we don’t see it that way. We are about to show you how this housing bubble is going to turn into a prolonged nasty housing bust. Which will then wallop government finances. And it will likely lead to a total political re-alignment in Canada, with voters desperate to pick any party that can turn this mess around. That will probably also involve things that are housing and government debt negative in the medium term.

In a word, Canada is a zero. It will start with real estate, but similar to Japan, the hangover will be felt across the country: government debt, equities, major banks and the currency.

Background on the Bubble

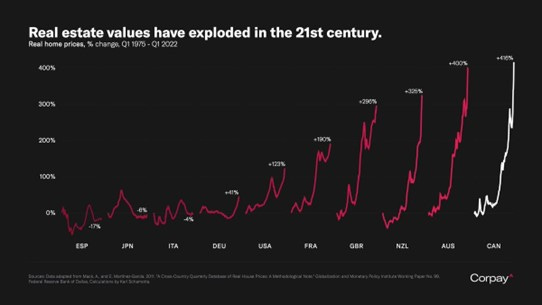

Housing prices have risen at such a rapid rate that it’s comparable only to major bubbles. Prices are up 425% since 2000, in real terms.

Viewed another way- Canada has passed every other housing market bubble that occurred in the last 30 years in the G10. The Spanish and US housing bubbles, and bust of 2002-2010, which crippled their banking systems, look mild in comparison.

Really the only thing comparable, historically speaking, is the Japanese real estate bubble in the 1980s, where prices from 1970 to 1991 went up 485%....

……before falling 45% in the subsequent 20 years!

Total private sector debt to GDP now exceeds Japan at its bubble peak

Affordability Is Nuts

One may justifiably counter –what’s the big deal with housing prices rising so rapidly, if incomes keep up? The answer is that they have not kept up. The rise in housing prices and the recent spike in mortgage rates has made housing in Canada totally unaffordable in the major cities.

wowa.ca

A brief detour to explain to our readers that the Canadian system works differently than the US in terms of mortgage financing. In the US, the vast majority of people take out fixed rate loans of long-term maturities – 15 to 30 years. Your payment is locked in on the first month and will stay basically unchanged the duration of the mortgage.

In Canada, the model works differently. People sign up for typically 20 year or 25 year amortization mortgages, but the interest rate is not locked in for that time period. Half of the market now is comprised of mortgages with an interest rate that is fixed but resets every five years. Variable rate mortgages, typically linked to a shorter term rate, comprise another 35%. The remainder are on fixed rates that reset every 2, 3, 4, or 7 years.

Another crucial difference is that US mortgages are mostly non-recourse, meaning that if the house ends up selling for less than the amount of the mortgage, the borrower is not on the hook for the difference. But in Canada, the lender has recourse to the borrower for years after the loss is generated. This fact makes real estate prices more volatile in the US in the short term, as people rush in or out of multiple properties, but it will make any down cycle in Canada FAR worse. Real estate investors in Toronto who own ten properties will have to continually adjust their finances or disinvest to cover losses generated by just one or two problem properties in their portfolio. In the US, they would only have to give back the keys on the overpriced/non-cash flowing properties and the bank would have to deal with the rest.

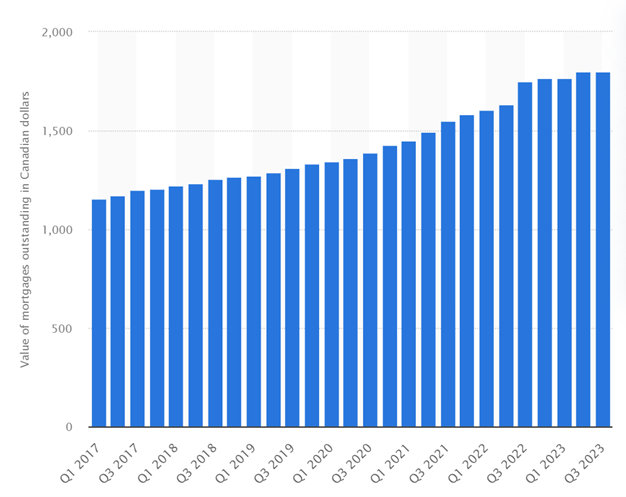

A net third of Canadian mortgages outstanding ($600bn) were newly issued during the prior five years period, and will now reset starting this year at far higher rates. Another large amount of mortgages, unknown in amount, had been renewing in the 2009-2022 period at low rates, and will soon renew at higher rates. The variable rate mortgages have been rising this whole time. So now almost two thirds of outstanding mortgages, and 100% of new credit, will bear the cost of this affordability crisis.

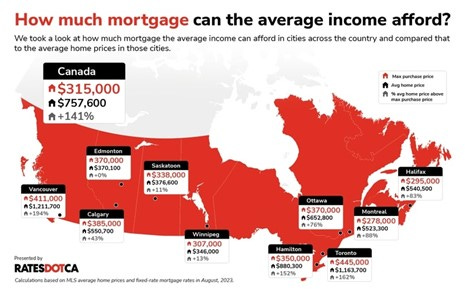

How Bad is it? On a national survey, it shows that average house prices are more than double what the average household can afford. This will require a long period of rising incomes and/or the air being let out of housing prices. We should also be fair and point out that the cities on the prairies are reasonably priced- Winnipeg, Saskatoon and Emonton will face no problems. But the coasts have an enormous bubble.

(all charts ratesdot.ca in this section)

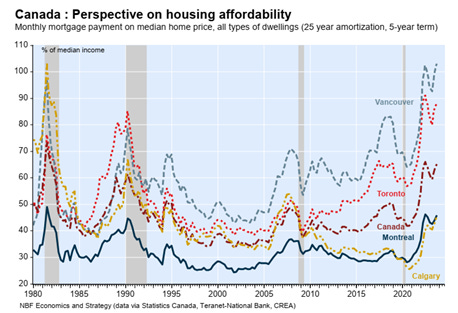

Housing affordability is the worst since the 1980’s, when mortgage rates were almost triple current rates!

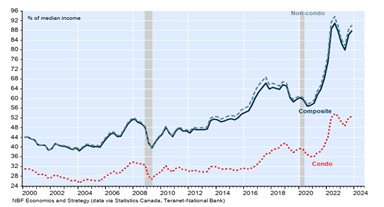

Buying in the largest, and not even the most expensive city, consumes an obscene amount of household income. Drilling down to the NBC data on Toronto specifically, we can see it’s basically impossible for the average household to buy a house – the average house would consume 90% of their income. A condo comes in only slightly better at 53% - versus personal finance guidelines of 20-33% for most people.

These have shot up massively in the past two decades (gray lines indicate recessions).

Weakening Economy

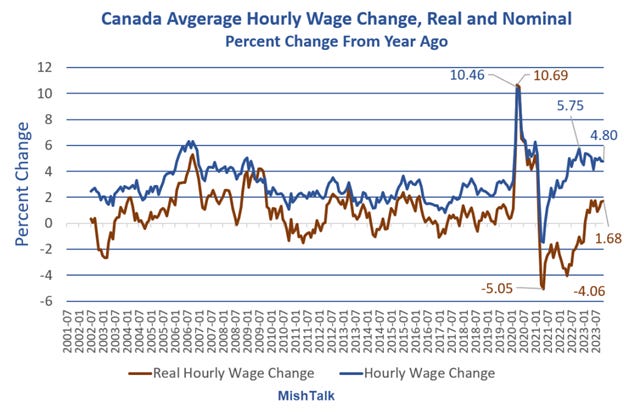

With super high housing prices and rising mortgage rates pinching affordability, you may hope that the Canadian incomes could grow their way out of the mess. Unfortunately, the data does not show that happening. Real wages are growing below 2%.

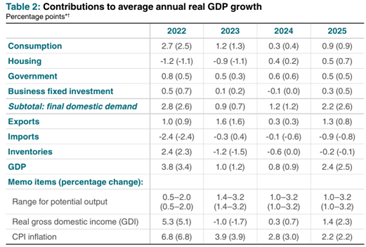

The Bank of Canada’s main report projects 1% GDP growth for 2023 and 2024, before a return to growth in 2025. We are worried that the housing issues could continue to suppress growth, creating a feedback loop of slow growth and a weak housing market.

BOC January 2024 Monetary Policy Report

Leverage Leaves No Room to Increase

Another valve to open would be to increase the leverage in the economy. The Chinese model for the 12 years after the Global Financial Crisis was to continually lever up and push property prices higher, until it all blew up in the past 18 months.

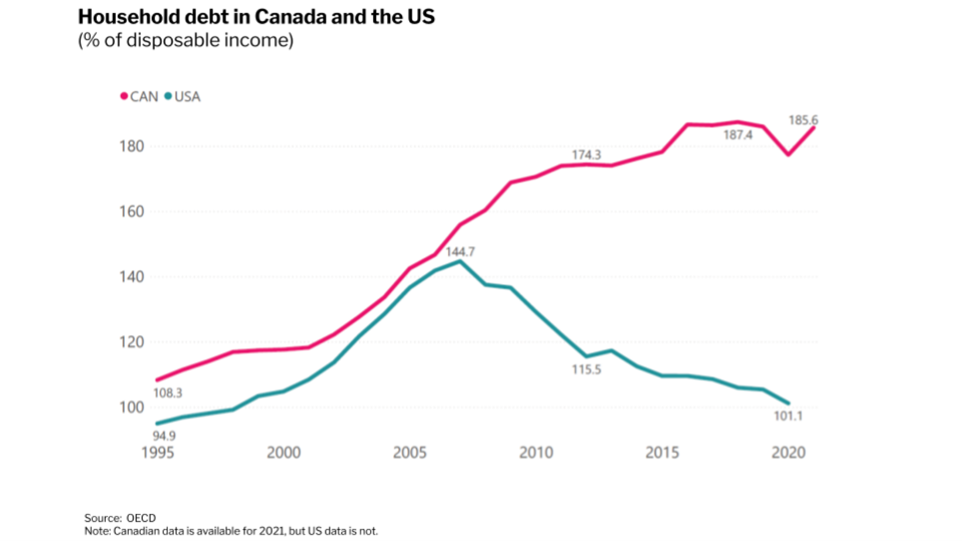

That is not currently an option for Canada, as the country has some of the highest debt levels ever seen in any country. The private sector debt to GDP is approaching 200%, a rate rarely seen for a long period in a major economy. Debt to income ratios rose in line with the United States until the 2008 crisis, and are now far higher on an absolute and relative basis. With the US arguably facing an echo housing bubble in several hot markets, Canadian household debt levels are almost double American levels!

The Rollover Has Begun

The Canadian market, along with others globally, have been expensive for the past several years. Several people called for a rollover years ago that never happened.

But now there is clear evidence that the rollover has begun. Both prices and sales started to turn down in 2022.

Wowa.ca

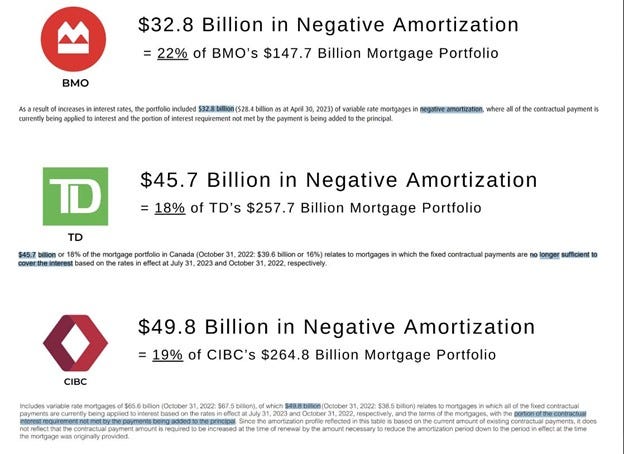

Now, by far the most ominous sign has appeared in the market. Mortgages where the borrower is unable to cover their monthly costs have gone from essentially zero to almost 20% of the total at major banks. The technical term for one when your mortgage principal amount grows each month instead of decreasing is known as ‘negative amortization’.

As we pointed out earlier, Canadian real estate is recourse. So an investor with a negative amortization property is faced with a difficult choice – sell now, or sell in the future for potentially a much bigger loss. Or downsize elsewhere to cover the balance. But when 1/5 are negative amortization with no prospect of rates falling, this is going to create a rush to the exit door across the housing market to deleverage. It’s often said that ‘forced selling creates crashes’, and it looks like a wave of forced selling is about hit.

Bank of Canada Response

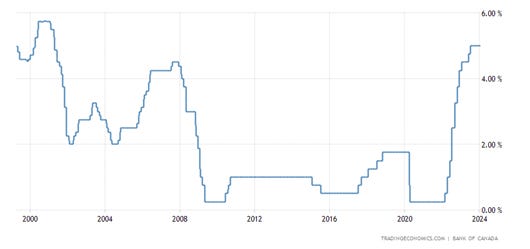

Another fairly reasonable question is- can’t the Bank of Canada cut rates? Won’t 200bps of rate cuts just cure this whole problem? Let’s dig into their rate policy and their balance sheet policy.

Bank of Canada Policy Rate

At this point, we are not betting on much of a cutting cycle to come in Canada and bail out housing. First of all, Canada strictly targets an inflation rate of 2%. Inflation is expected to be 2.8% this year and get to 2.2% next year on official forecasts. That realistically leaves room for one, maybe two cuts in 2024, and potentially a larger easing cycle in the second half of next year. Based on their forecasts.

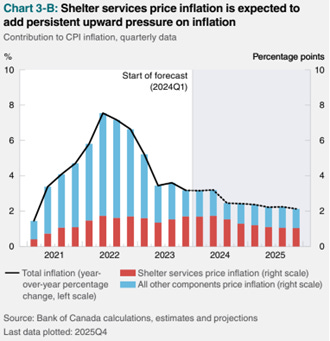

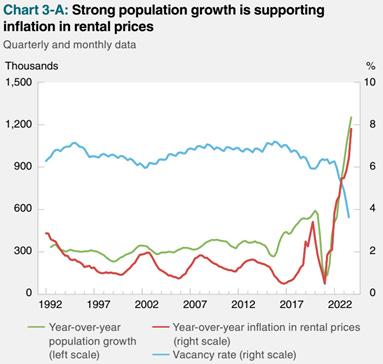

But core inflation continues to be strong, and come in higher than expected. Paradoxically, it’s driven by rents! As Canadians got priced out of being able to buy a home, they moved into rentals. And they’ve had to compete with immigrants. As rents rise, shelter inflation rises. The government expects shelter inflation to level off, despite rents yoy reaching new highs. We think they are overly optimistic. So this dynamic may prevent a large rate cutting cycle as core inflation prevents overall inflation from declining to 2% or lower.

BOC January 2024 Monetary Policy Report

At this point, in debating whether the BoC is done hiking or not, we want investors to focus on the big picture. Rates went from being sub 2% for almost 15 years to their current 5%. That’s the highest in 21 years. And this is in a market where mortgages typically reset every 3-5 years. All the price to income, loan to value, monthly payment to rent numbers that worked at 1.5% rates will have to be greatly adjusted. And that adjustment is going to be one of lower housing prices.

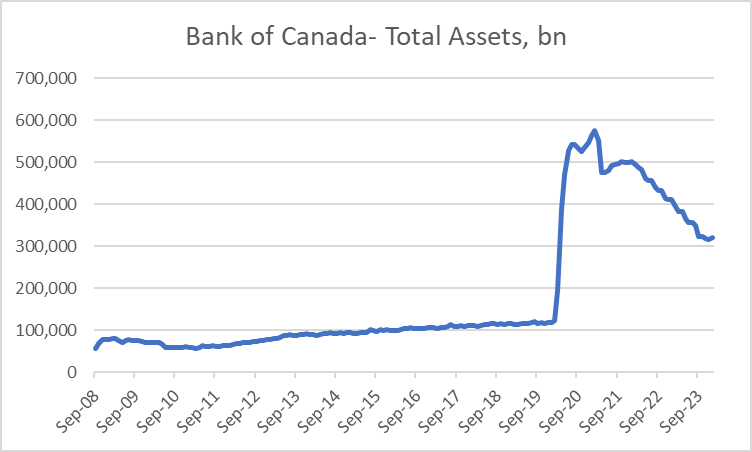

The last question would then be- could the Bank of Canada just do QE? The data shows the opposite. The BoC flooded the system with liquidity post COVID. But it’s largely let all that roll off, and its balance sheet has decreased by 45% in the past two years. That will not help the credit situation.

Source: Bank of Canada data

Immigration and Housing

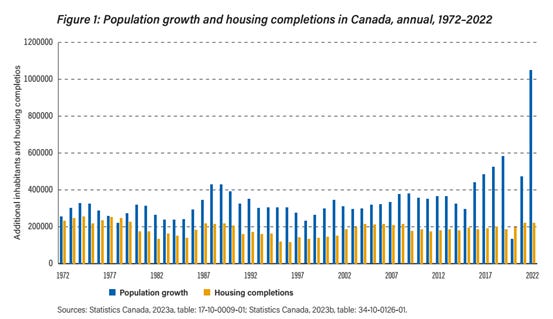

Another part of the bullish housing story has been the number of immigrants to Canada. The population has indeed been growing at the pace of 1% or more per year. The country of 40 million has routinely let in 400k-500k immigrants per year, and recently crossed 1m immigrants annually.

Fraser Research

The government has faced a lot of backlash on this policy, for several reasons. The increase in housing prices and rents has made it unpopular. The government has faced a lot of pressure, and is now expected to begin to curtail the influx.

People Still Smoking the Hopium

We are big believers in the fact that the markets are driven by sentiment. If Canadian investors were in despair, swearing off real estate as an asset class and cursing the Bank of Canada, our bullish antenna would pop up. But the sentiment reality now is the opposite. Participants are desperate for things to stabilize and are definitely ‘smoking the hopium’. They think immigrants or the Bank of Canada will bail out their wildly overpriced real estate holdings.

Of course, we point out, that they wrote the same thing last year!

This unrealistically optimistic sentiment coupled with the facts we laid out earlier on immigration, affordability, and the Bank of Canada not able to save the day will create a long, brutal bear market.

Government Finances

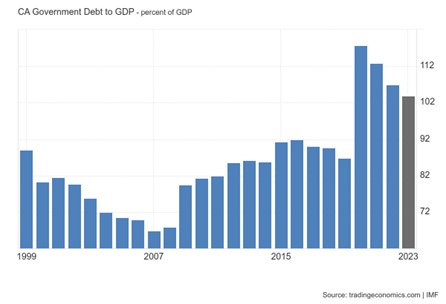

The last option would be for a central government stimulus plan, which would spend their way out of this. The government in Canada runs a relatively modest 1.5% of GDP deficit, which is low by developed world standards. But its debt to GDP is over 100%, which gives the country limited room to increase the debt levels sustainably over the next five to seven years. This fiscal constraint is going to prevent the government from stimulating now. And in the future, it would probably rise as the government begins to bail out banks and government affiliates suffering from the housing bust.

Political Inflection Point

All of these economic rumblings have finally begun to hit the ruling Liberal government, led by Justin Trudeau.

Source: Wikipedia

Trudeau became the leader of the Liberals in 2013, and then prime minister in 2015. He has ruled for the past nine year and has won three elections. He now runs the government in coalition with the New Democratic Party (NDP) – Trudeau’s party has 157 seats and the NDP has 25.

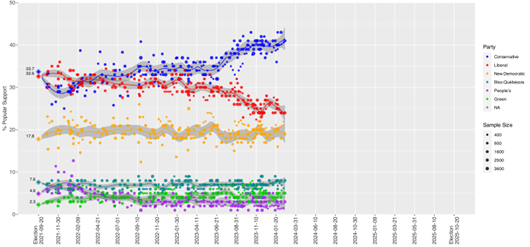

But polling shows a huge hit to the incumbent government in the last nine months. The polls show that the Liberals’ vote intention has slipped rapidly from 33% to 23% in the past year as the economy deteriorated. Meanwhile, the conservates are now over 40%:

Source: Wikipedia

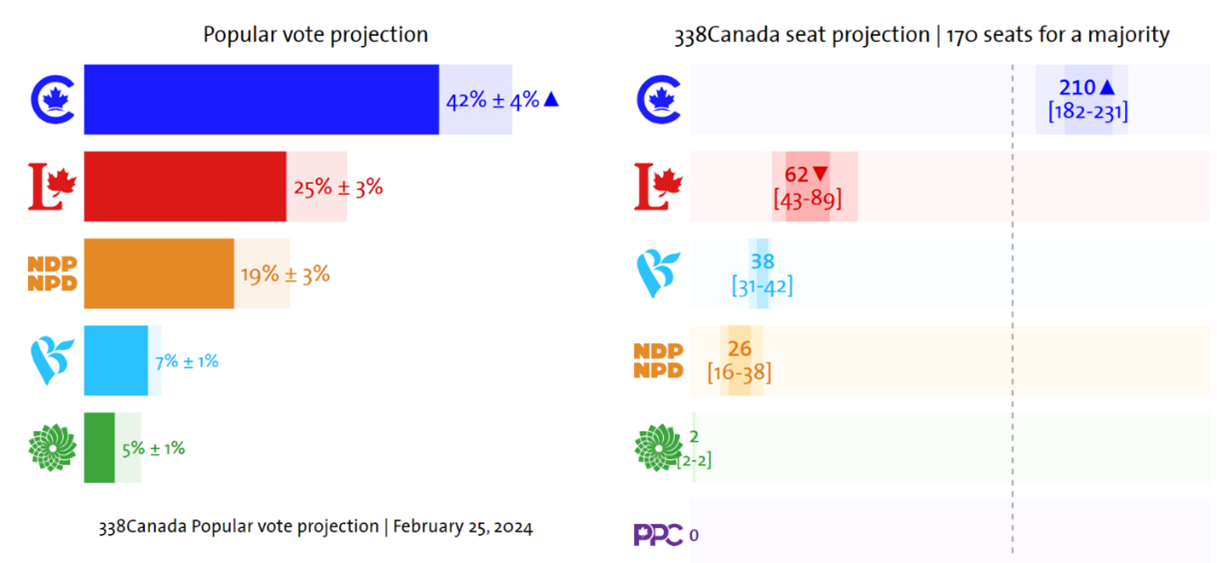

This will translate into a strong Conservative majority in terms of seats, with around 210/338 seats.

But this is early in the economic crisis. The election has to be held in the next 18 months, before October 2025. As the banking and housing crisis deteriorates over the next year, we anticipate Canada’s Liberals will turn into an equivalent of the UK Conservative party and face a total wipeout.

It’s a safe to say that the Conservatives will roll back many of the Liberals’ now unpopular policies, much of them housing related. We can foresee the adoption of three or four out of the items on this list in the next few years. These will not be housing market friendly:

1) Curtailing Immigration. Given the high numbers of immigrants, their contribution to high housing prices, and the abuse of the system, further rollbacks in immigration are highly likely.

2) Some sort of nationwide forbearance, mortgage relief or other government support. Expect Conservatives to blame predatory banks and the previous administration for entrapping the average citizen. They will probably tax banks or reduce their profits by allowing all manner of restructured payments, reduced costs, debt relief etc. This will keep current homeowners in their houses, but will hurt banks and future bank credit.

3) Far More Building Permits. As we saw earlier, immigration alone has far outpaced the number of building starts. There will inevitably be a push to expand construction and push down prices.

4) Crackdowns on Foreign Purchases, Money. In response to tons of high-end property being bought by unknown foreign entities and buyers, the US in 2016 passed new disclosure laws. These had the deterrent effect of scaring off these large foreign buyers, and as a result many hot markets like NY, LA and Silicon Valley permanently cooled off.

Given the concerns over corruption and money laundering into Canadian property, most of it coming from China, expect a whole new crackdown.

“But Decoding, Canada already banned foreign purchases in 2023! For Two Years!”

Yes, we are aware. But that law was largely toothless. It exempted temporary residents and permanent residents. And it left a large grey area open for corporations, who have been driving the vast majority of the high-end purchases in Canada.

We expect crackdowns and new disclosure laws on all sorts of property transactions done in the past that will put pressure on the market.

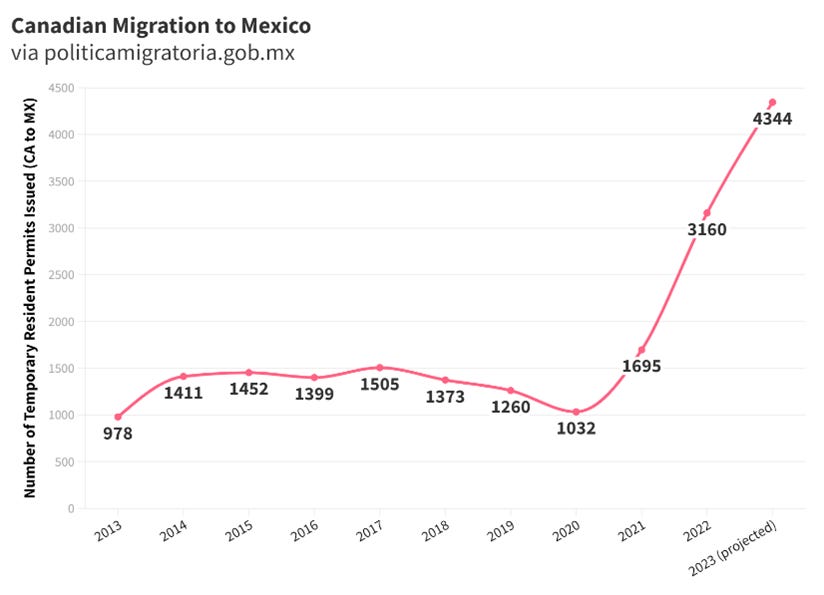

5)Canadians Move Out. As of now, the overall quarterly rates of emigration of Canadians remain unchanged from pre-pandemic. But given the grumbling of Canadians online and the difficult economy, we would not be surprised to see it pick up. We think that certain countries, where the cost of living is much lower, will be the beneficiaries and the leading indicators. Mexico is a great example, with the number of Canadians issued residency permits up 4x in five years.

We think the Canadians moving to Mexico trend will pick up rapidly, as they cash in Toronto apartments for beach-side villas in Puerto Vallarta. The last time we were in Mexico’s coast, we were stunned by the amount of cars with Canadian plates. Maybe they’re just vacation homes now, but we’d not be surprised if they become permanent homes soon.

Who Takes the Loss?

Our next piece on this ugly topic will be to explore this theme in more depth. But we want to point that out in ugly housing busts, non-performing loans routinely go to very high levels. It could be anywhere from 5%-7% of system loans like in the GFC in America, to the 15-20% levels seen post bubbles like Ireland, Spain, Greece and Japan. So with that in mind, we think Canada is going to end up with at least 15% of system mortgage loans defaulting, generating a loss of $200 or $300bn. Having 20% of system loans already in negative amortization is a potent warning sign though that this could be one for the record books. And given the vast amount of other loans that are used as mortgage debt (home equity lending, etc.) we will probably have to greatly increase the losses beyond mortgages to get the total amounts.

Shadow lenders are going to be in deep trouble. The major banks will face a river of losses. The government’s insurance body, CMHC, is going to need a massive capital injection – it currently has $900bn in guarantees and less than $25bn in capital. And the upcoming several years of weak economic growth and bailing out housing losses will strain Canadian government finances.

Sorry to tell our dear readers in the Great White North, but Canada is a Zero.