June 2026 – This Year’s Dot Com Bust

Comparing the similarities to March 2020 as the Tech Boom Inflects

Email: decodingpolitics@protonmail.com

Substack: decodingpolitics.substack.com

Twitter: twitter.com/DecodingPoliti2

*Not financial advice, merely pointing out political and macro trends*

“There is nothing new in Wall Street. There can’t be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again.” – Jesse Livermore

The US markets, notwithstanding the speed bump of March, had a good year through Wednesday June 3rd: The S&P 500 was up 11%, the Nasdaq 100 was up 20%. A good year in six months.

That appears to have inflected on Friday June 5th with a big selloff across the board. We have been working on this piece for a while and unfortunately did not get it out before the first drop. But we are still warning you in the strongest terms: The markets of June 2026 strongly resemble the markets of March 2000. That month ended the mania of PC/dot-com/large cap tech stocks of the 1990’s. What followed was a three year bear market and an 80% drawdown in the NASDAQ.

We don’t think that the scenario will play out exactly the same. Yet having been around the markets at that point and now, the parallels are uncanny. We are going to go through the similarities of the two environments. We will tell you what happened to major tech stocks in 2000 (hint: it was ugly) and thus likely to the tech darlings of 2026. Copying out all the charts and relevant news articles would take this to way longer than we desire- but we give you all the names and key turning points to do the research yourself.

We were bearish in January, bullish in early April, and turned neutral in late April. This was all on the Iran war. But the market no longer focuses on that- on June 5th the Iranians withdrew from all negotiations, fired missiles and oil ended up down $5 on the day. The market has now moved on to AI dynamics.

We are now cautious on US and global markets. We are now extremely cautious on US tech and other tech heavy, levered markets. Korea is probably the prime example. Please note, we are not calling for a general market crash or a down 50% bear market in the S&P.

But we are fairly certain that a lot of air is going to come out of the bubble that has been inflated in tech, memory, semis, AI infrastructure and other pockets of the market that have seen a speculative frenzy. The memory of the brutality of the dot-com bust and the ease of just going into various hiding places implores us to tell you to be cautious and re-allocate.

We will break down this piece into a few pieces:

1) The 1990’s into 2000….And Afterwards

2) The Market in 2026

3) Just Like 2000, Supply Will Bury The Market

4) Parallels Are Uncanny- Valuations, Retail Trading, Saylor, Buffett

5) Likely Roadmap

6) The Game Plan

1) The 1990’s into 2000….And Afterwards

The 1990’s were fundamentally the most bullish decade since the 1920’s. The Cold War ended in 1991, generating the ‘peace dividend’. New markets in Russia, China, and India opened up. NAFTA promised to boost trade with Mexico and Canada. Interest rates and inflation were low. Politics were moderate domestically.

It was also a time of technological progress. PC’s went from a niche product to every desk and home. Mobile phones went from a funny accessory in the movie ‘Wall Street’ to widely adopted. The Internet went from an obscure government computer network to connecting hundreds of millions of people globally.

Initially, the companies behind this rode the strong adoption and growth to continue growing. A broader retail investor base, with online trading and broad access to mutual funds, was happy to buy them. There was nothing super speculative about it until 1995.

That was when the first real Internet only company, Netscape, IPO’d. It was a small loss making company, but it also had created the first browser to use the World Wide Web. It was the first product that made the hard-to-access Internet of yore easy and scrollable to any grandmother. Interest in the product and company exploded. The stock went crazy. After that, the floodgates opened and hundreds of new companies came to market each year.

By 1999, the Dow Jones Industrials had gone from 1,000 in the early 1980’s to 10,000. Analysts called for Dow 36,000 soon [the author of that book serves in the White House now] Tech stocks and indices performed vastly better. Companies found that rebranding as .com or Internet businesses saw their stocks re-rate like crazy. The demand for telecom equipment to build out networks to support mobile and the Internet was huge. 1998 and 1999 saw a flood of ‘dot-com’ businesses hit the market, hundreds of new businesses, mostly loss-making. The mania built and built in 1999 and early 2000.The NASDAQ doubled from October 1999 to March 2000 (very similar to the rally since Liberation Day 2025).

The market hit its peak in March 10,2000. It sold off a few days, no big deal. It reached a new high (Nasdaq 100) and matched the high (Nasdaq Composite) two weeks later. After that, it went into a tail spin and declined roughly 40% in eight weeks. The Nasdaq 100 ETF, ticker QQQ, went from a high of 120 on March 24th to a low of 72 on May 24th. That’s 40% in 8 weeks.

After that initial bust, QQQ rallied back to 100. It finished the year at 60. From there, the market stair stepped lower over the next two years, with QQQ bottoming at 20 in October 2002.

QQQ: October 1999 to October 2003

Hundreds of stocks went down 90% or more. Many marquee businesses went bust. Retail investors were hammered. Reports of people who had made a fortune day trading and then lost everything were common. It turned out that debt levels and valuation levels had reached the highest levels in 80 years during the 1999-2000 period, leaving no room for error. When the errors happened, speculative stocks blew up.

2) The Market in 2026

We all know the story: AI is going to change everything. The data center buildout is beyond huge. GPU’s for everything. Now it’s going to space, into every industry, and its going to begin programming itself and achieving hyper-growth. And the race is on for the first company to achieve AGI, as they will be the winner.

The dynamic is similar to the Internet bubble. A new revolutionary technology [the early Internet]. It will displace everything else [online shopping, newspapers, post offices] and enable many new industries [radio and video streaming, shared working] A massive infrastructure build is necessary to get to scale, and winner takes all.

There was a giant buildout of everything telecom- new mobile networks, new Internet connectivity like T-1s and ISDN lines and cable modems. There was huge spend in new fiber optics and mobile networks, equipment to power them, data centers, switching hubs, routers and all the nuts and bolt of Internet architecture. Many of the big spenders on fiber promised huge things and went bankrupt- Level 3, Qwest, Global Crossing, and Worldcom.

There were revolutionary technologies in the past two decades- smart phones, social media, EV’s. Why weren’t those bubbles too? Those stocks just kept growing despite what the haters say. Those businesses were our early 1990s PC and mobile companies: steady growth, cash flow, and predictable adoption curves. No debt, no negative FCF, no speculative hoopla.

The reason we think it’s a bubble now similar to 2000 but was not in past years is based around three simple facts. One, at the end of the bubble businesses that were consuming capital were the focus, not the good growing and cash flowing businesses. When the external capital hit the pause button it was over. Then it was dot-coms and telecom companies – now it’s AI scalers. Secondly, in 2000 there was massive supply of new equities, from both new and existing companies. Tons of smaller dot coms and network companies hit the markets in that period, and many major companies IPO’d or were spun off: Palm and AT&T Wireless most prominently. Finally, the tech sector had reached such a large part of US and global portfolios that it had pushed valuations to ridiculous levels and pushed investors into a position where they had to sell and rebalance.

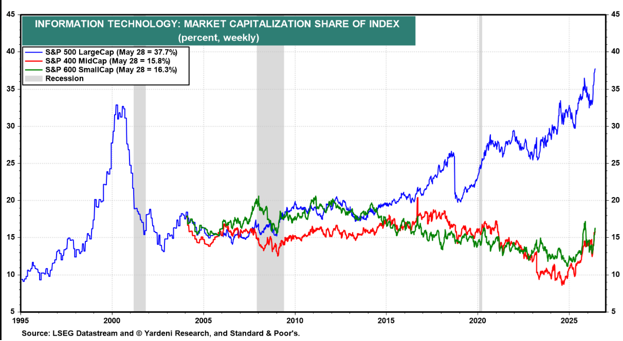

The huge concentration in the 1990’s was in stocks obvious to all: Nokia, Dell, Microsoft, Intel, America Online, Cisco Systems, Sun MicroSystems, Nortel and Lucent. Ciena, JDS Uniphase and Qualcomm were the growth plays. Ebay and Amazon for e-ecommerce. If you wanted a holding company of these, businesses you bought CMGI or Internet Capital Group. Tech was almost 33% of the S&P in Q1 2000. One fund manager, Janus, took in half the inflows at one point by building huge positions in those stocks. It became a forced seller for years when the market turned.

Longer term what happened to these names (say a decade later). America Online merged with Time Warner and the stock went down massively. Nokia, Nortel, Lucent were basically out of business along with so many other telecom companies. Sun Micro, Intel, and Cisco had 80% drawdowns but survived and remain below their 2000 highs. Dell had a similar fall and went private again later on. Amazon, Qualcomm and Microsoft all eventually exceeded their prior highs, but took massive drawdowns and a decade+ to do it.

Now it’s obvious to own the Mag 7 – Nvidia, Apple, Alphabet, Microsoft, Amazon, Meta, Tesla. The forthcoming Spacex, Anthropic, and Open AI offerings created feeding frenzies the past few quarters in private markets. The memory and semiconductor industries are considered no brainers to capitalize on the multi-trillion dollar secular growth of AI and data centers. Investors appear to have forgotten that these two of the most cyclical industries on earth, and this time around, they are carrying far more political risk than before. Tech is nearly 40% of the S&P depending on how you count it.

We will discuss more in the aftermath section but we want you to keep in mind one thing. There is no doubt all of these were transformative businesses and technologies. They generated great returns for a long period of time. But eventually, stock prices reflected wildly overly optimistic assumptions relative to what would play out, and they turned into terrible investments over the next ten years (or are likely to).

3) Supply Will Bury The Market

The 1999 market as we mentioned featured a tsunami of IPOs. Those came largely in the second half of 1999 and early 2000. Many insiders were locked up from selling for 90 or 180 days. But when the window opened for executives to sell shares, they took advantage. With so many companies and so much stock for sale, it eventually turned out to be too much to handle. When retail sat on their hands or joined in the selling, there was no one left on the other side. Tons of stocks crashed post IPO lockup windows.

Several fortunes were made from shorting these weak links. Legendary value investor John Templeton was famous as a stock picker, not a short seller. But he saw the opportunity as so irresistible that in January 2000 he put on a big basket short in these companies. A Forbes article from 2001 did a great job breaking down the trade and the reasoning and timing behind it:

“Templeton, however, arranged his short-position schedule with his broker in January 2000, when techs were hot. Gains thus far: $86 million.

Templeton slated his short positions to take effect 11 days before lockup expirations—that point, usually six months after an initial public offering, when insiders are allowed to sell their stock. He focused on tech shares selling at three times the price set in the initial offering, rightly figuring company insiders would cash out some of their absurdly valued holdings, putting downward pressure on stock he suspected was due to fall anyway. “Insider selling was the trigger but not the main driving force,” he says.

He shorted 84 Nasdaq stocks, taking positions averaging $2.2 million each. In nearly half of the shorts he waited until prices dropped to 5% of what he paid, thereby cleaning up on such names as Foundry Networks, Breakaway Solutions and Vitria Technology (see table, above). At other times he closed out his positions once the stock price dipped below 30 times trailing earnings. He took losses early, quickly covering positions where the stock price increased post-lockup.

The 2026 market is looking to be one also chock full of supply. Numerous pundits have said only the 1999-2000 market can compare for issuance relative to the size of the market. Already out the door are two big tech firms, with a third likely to follow.

Oracle already announced a $20bn offering in February. Rumors are more is needed.

Google announced a $60bn last month.

On June 5th, speculation hit the market Meta was next for tens of billions

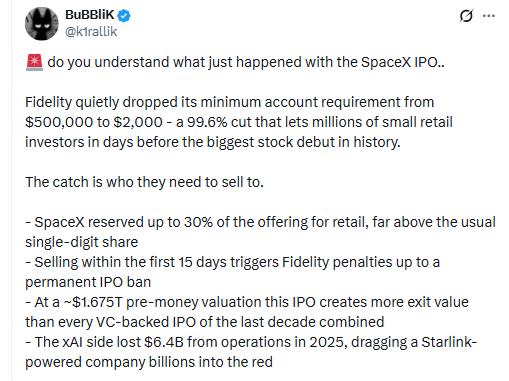

Then there are the upcoming IPOs. The big daddy is the SpaceX deal. If it prices at the likely IPO price, it would be worth over $2tn. That would make it third largest market cap in the entire market at IPO. At least $60bn of that is primary.

Soon after, the market will see deals from two $700-900bn range companies, Anthropic and OpenAI. Our suspicion is the latter deal actually may not happen. There are many, many things that do not add up at Open AI. Similar to WeWork, putting the numbers down in an S-1 may be the end of the story. But that’s for another article.

To say nothing of the myriad smaller players and secondary offerings. This is, by our back of the envelope going to be probably $300-400bn of primary shares offered and much more potentially in secondary selling. Those are big numbers!

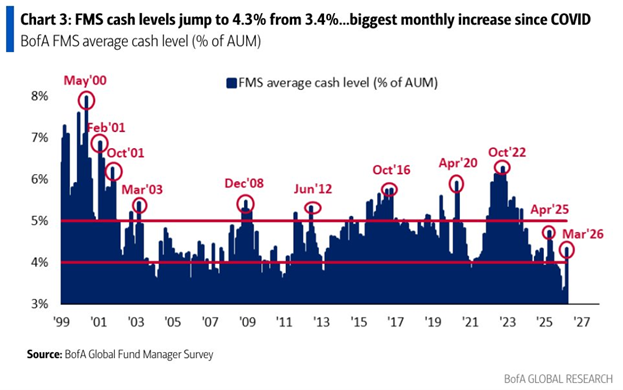

It would be one thing if all of this stock was hitting when fund managers had lots of cash to buy it like in 2012 or 2022. But it’s the opposite! Levels are near the lowest in history. This data is from March, and we are sure it’s lower now in the first week of June after the big run-up:

Lots of new stock, not a lot of capital to purchase it, is the Econ 101 way you get lower prices.

Finally, there’s the index dynamic. They changed the rules so that after the first 15 trading days, SpaceX can cruise into the Nasdaq and FTSE indices. Great, more buyers, right? Well that’s half the battle. Index funds will have to sell other names in order to raise the capital to buy SpaceX, as by definition index funds run with almost no cash balance. SpaceX is likely to coming in at a 5-7% weighting in the Nasdaq 100 index. That’s going to be a whole lot of selling in the Mag 7 and the other names that track the index. Three of those big Nasdaq 100 names, as we pointed out, are also issuing or have issued new shares.

Who will be on the other side of all of this rebalance selling? Or are we just setting up an environment for a new Templeton trade of shorting all these?

4) Parallels are Uncanny

Not only are the structural drives and the price performance similar, there are a very uncanny echoes of 2000 that only seem to emerge at turning points like this. As Livermore said, there is nothing new in the stock market. Not only is the structural setup very similar, even certain little market happenings are showing you how similar these two dates are.

Valuation

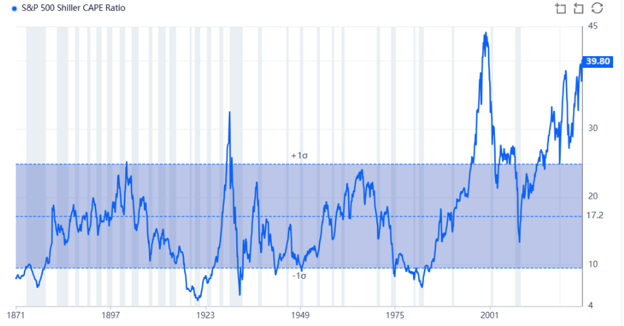

The continued price performance of the Mag 7 among others has created a tremendous valuation extreme. We showed the share of IT in the S&P earlier had hit all time highs. On a ten year PE basis, such an extreme has only been hit once: in March 2000

Again, people rationalized paying absurd, above 1929, levels. One line from the Templeton article we previously cited made us chuckle- if only he could see 2026 valuations!

Like other value investors, he was agog at the market’s frothiness. “This is the only time in my 88 years when I saw technology stocks go to 100 times earnings; or, when there were no earnings, 20 times sales,” says Templeton. “It was insane, and I took advantage of the temporary insanity.”

How bad is it to pay high prices 10-20x sales, or 40x earnings for the S&P? We previously cited Sun Mircosystems as one of the highfliers that crashed. There is a great story from 2002 where the CEO questioned what on earth investors were doing to bid the stock up to a (then) irrational 10x sales:

“During a March 31st, 2002 interview Sun Microsystems ( SUNW ) CEO Scott McNealy said this about his companies valuation.

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64?

Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

This just shows you how exactly right you have to be on the growth trajectory, and its profitability, for current valuations in big cap tech and speculative names to work.

“Buffett’s An Idiot!”

At the end of 1999, tech stocks continued to soar while Warren Buffett’s holding company Berkshire Hathaway was down on the year. Criticism was heaped on that he was out of touch and only invested in the old economy. His methodology didn’t work any more. Here was a prominent article in Barron’s from December 1999:

Would you believe it, the greatest investor of all time bounced back and lapped the market over coming years.

With tech stocks ripping and Berkshire moribound, the same criticism has come back around in 2026. As Buffett has held onto a $350bn cash position, people are criticizing him again:

A desire for speculation and an eschewing of the quintessential safe investment is once again happening likely at a key inflection point.

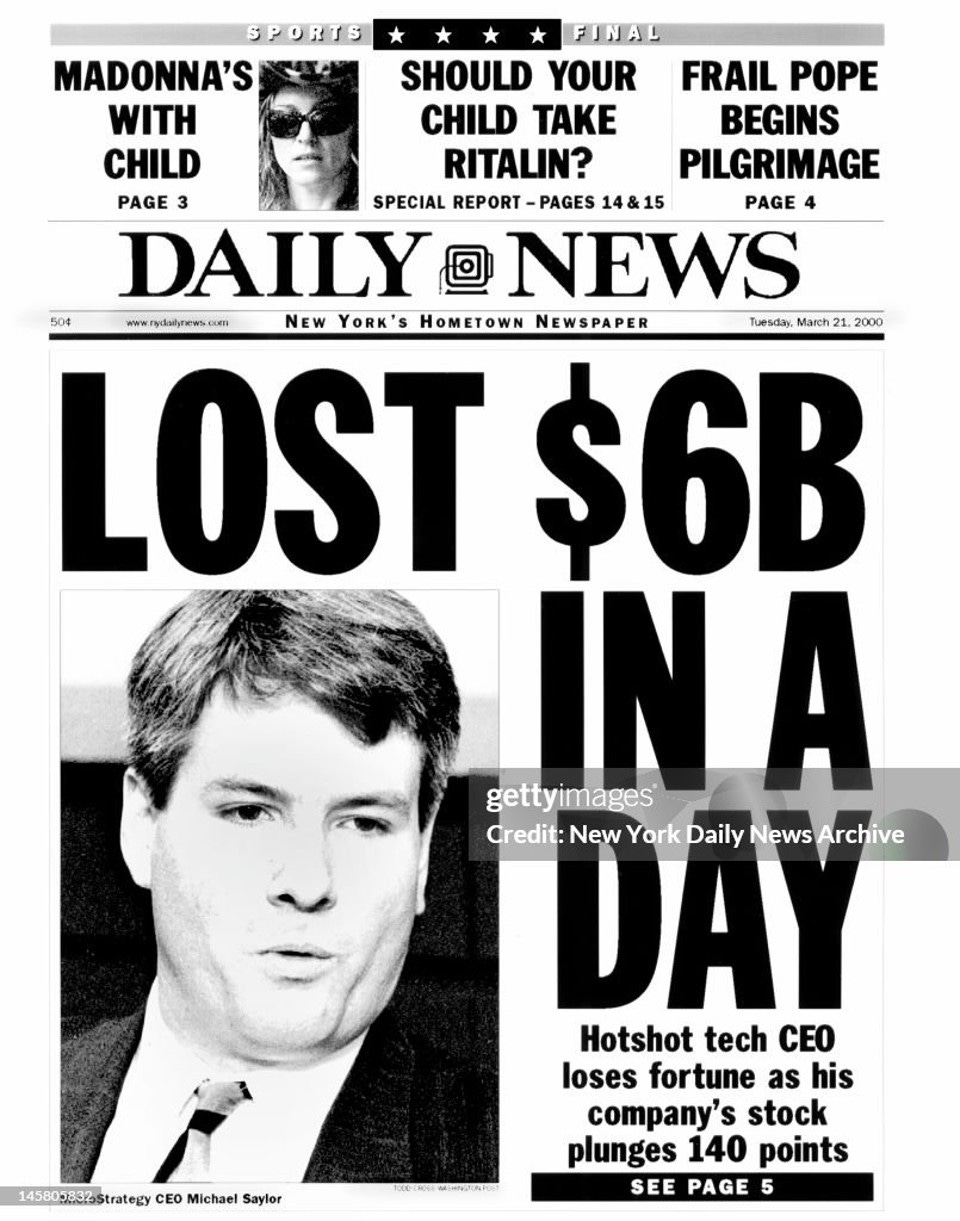

Michael Saylor Blows Up

Over the past few years Michael Saylor has emerged as perhaps the leading voice of the Bitcoin movement. He went from having an obscure software company to possessing the largest Bitcoin Treasury company on the planet, Strategy. That company has $64bn of BTC at cost. The stock is down about 70% from its high and is falling. There are starting to be rumors in the market that Saylor will have trouble meeting interest payments, sell his Bitcoin, or that the creditors may be able to move in on him. He has now lost $13bn on his bitcoin and counting, having accumulated it sloppily over the past six years:

We don’t know the mechanics- but we do we know that he was in a similar position in March 2000.

“What’s that?” you ask. Well in 1998 – 2000 Saylor had been a high flying tech CEO at the first iteration of Microstrategy. The stock had mooned and he was worth billions. On March 20, 2000, it emerged that the company had improperly recognized revenues. The SEC had begun an investigation and it looked like they would have to restate earnings and declare a loss. The stock crashed. It ended up the Internet bust 99% off of its highs.

Later on, in a separate case he had to face claims of tax evasion for claiming he lived outside Washington while maintaining a home and partying it up in Georgetown. He paid a fine.

He now lives in Miami Beach, in a compound visible to all with multiple houses, yachts parked outside and a new jet on the way as his stock crashes. Leopards never change their spots!

Two things here. One, it’s an uncanny parallel of how speculative the market has become yet again. And secondly, we understand being bullish on Bitcoin, but this is not the horse you want to ride.

Companies Riding the Wave

In the 1999 bubble, countless companies rolled out a website, rebranded as an Internet company or they added dot.com to their name. It produced a pop almost immediately. Now companies are doing it with AI. We think the funniest example of this is Allbirds. This was a wool shoe company which was a favorite of Silicon Valley entrepreneurs. The stock had been underperforming over the past year- so why not become an AI company?

Day Trading/Retail Participation

There was a sea of retail day trading in the late 1990s as investors chased performance and capitalized on the lax brokerage laws around it. Internet trading made it easier than ever. Countless publications featured rags to riches stories. After the dot-com bust, the day traders took the blame. The SEC overhauled the rules. They limited the number of day trades one could do, the amount of equity you had to have, and the disclosures. Day trading was seemingly under control again.

Except now it’s back! The government is the ultimate engine of consensus, and we suppose now that the government thinks the coast is clear from those day traders who blew themselves up and the market in 2000.

Schwab

Expanded retail participation is another. E-trade and others allowed cheap online trading. Index funds allowed cheap, passive participation. Tons of new people entered the market and bragged about how much they were making. There was no reddit then, but 1999 era WSB threads would have been great time capsules! We won’t put anything here, books have been written with all the great stories of retail froth. It got so bad that in “Mission Impossible 2”, released in May 2000, the villain eschewed cash or gold or diamonds for…..options in biotech shares.

Another interesting trend that tracks from 2000 is the rush to participate in IPOs. These were the hottest stocks at the time, sometimes rising 500-600% on their first days. Retail was largely shut out and pounded on the doors for the process to be democratized. Several brokerages opened up the process in the end.

Now the process is repeating with the mighty SpaceX IPO. Retail investors down to account values of $2000, from $500k formerly:

On the one hand, this may look like democratizing the process. Sadly, we will be more cynical and we think it’s opening up more and more investors to be on the other side of exiting SpaceX holders.

Retail participation is a hallmark of bubbles. When you see people who shouldn’t be trading stocks doing it and bragging, run. Joe Kennedy famously sold everything in the summer of 1929 when the shoe shine boy gave him a stock tip. And our favorite remains the CNBC special on retail investing in China in their bubble of 2015- it had a video of a remote village where the villagers lined up 30 deep to use the one computer in the whole village to check their portfolios and day trade, 5 minutes at a time. You can guess what happened soon after.

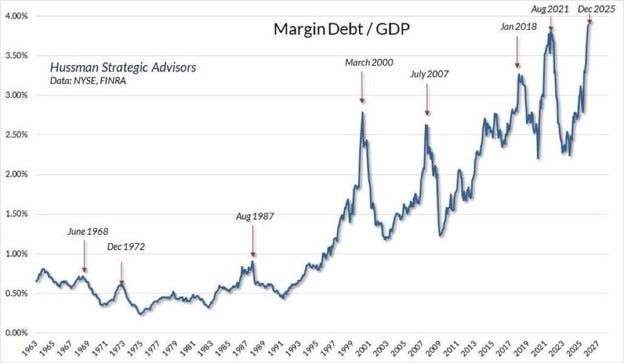

Margin debt is a reliable indicator of retail enthusiasm. A big run up usually precedes a big correction, and we imagine it’s even worse as of June 2026:

Naturally, all these untrained and overlevered newbie investors will be left holding the bag.

5) Likely Roadmap

The market’s hottest sectors are likely a bubble. Is it likely to end soon? But how soon? And for how long?

We think that the market will be, similar to March 2000, in a topping process for the next few weeks. We see the weakest links headed lower first. Some stocks may make new highs. But stocks should be in a range trade with a downside bias for the next three weeks or so.

But the market won’t crack yet. The big institutions need the Google sale, the Meta sale, and the SpaceX IPO to ‘work’. They and their clients will rush in after to big down days to try and put in a floor. The same thing happened in 1929, where after the initial breaks, pools formed in large names to keep them propped up. It will probably work in preventing a real bust for a couple weeks.

Zooming into the Nasdaq in March 2000. The composite peaked in March 10th and on March 14th had its first big down day. It was lower the 15th and the 16th. It found a range and traded higher, making a lower high on March 24th. The Nasdaq 100 hit a new high that day. After that, the wheels came off. This implies that we hold up until say June 22nd before commencing a big liquidation.

QQQ: Feb 1, 2000 to May 31,2000

Yet, as we laid out in the supply section, the amount of stock being unlocked will become enormous by the first week of July. Index funds will have massive amounts of Nasdaq winners to dump for SpaceX. The amount of SpaceX for sale the moment it’s in the Nasdaq 100 and FTSE will be big, and grow every two weeks. Those who worked there for fifteen years and can now cash out some will gladly do it.

Once this breaks, leveraged mega hedge funds will have to take down risk. That will send shorted stocks higher and the hedge fund favorite Mag7 lower, creating volatile trading in everything. Retail will panic and many will be forced to liquidate by their broker.

Medium term 3-24 months, the market will reprice these stocks to reality. But it might take the wind out of the sails of the broader market for only a few months.

We expect a summer break in all these tech names- the reason will be found after the bust. Further weakness could carry into say October or January. From there, let’s see where we are in valuations and sentiment. The latter is far more important. In our many years of doing this, there is only one sure sign of the end of a bear market. It has nothing to do with valuations, policy changes, interest rates, earnings or anything else. Nope, the sure fire sign a bear market is over is when investors are all miserable and most have left the table. Then all the sellers are out or nearly out, and a small amount of new capital can turn things around.

6) The Game Plan

“Impressive, Decoding, I didn’t know how similar the two tapes were” you may be thinking. “But what should I do?”

This is not financial advice obviously. In markets where prices have large runs like the Nasdaq recently, it never hurts to take money off the table. You may miss some future upside, but it never hurts to put money away and wait for a clearer picture. But if you knew there was a risk for a quick sustained break to the downside, as seems likely for later this summer, here are a few things we would consider.

First, if you have portfolio leverage, reduce it now. A fast break with margin will crush your account balance. 50% down in your stocks in a 2x levered account is a total loss of your money.

Secondly, reduce exposure to names that a) way overvalued b) have leverage c) have leveraged shareholder bases. When things get uncertain, these tend to get hit the hardest. Try to find the windows where insider selling could crush something you hold and exit ahead of it.

Thirdly, take a close look at defensive and boring companies. 10x earnings, steady growth and a dividend is pretty dull in a world of 100% growth at 100x earnings. But when the cycle inverts, it’s a nice place to hide. You don’t have to worry about IPO lockups in Johnson&Johnson.

This trade worked extremely well in 2000. Pharma companies bottomed the same week that tech stocks topped. Then they had an enormous rally of 50% in nine months while the S&P and NASDAQ tanked. Any fund manager long these had huge alpha over the indices. We are not saying now necessarily to buy pharma. But what we are saying now is that there are plenty of beaten down, forgotten, ignored segments of the market that can see a nice rally as the tech bubble inflects. Look out for those and spare yourself guessing where the bottom in Palantir is.

DRG (Pharma) Index October 1999-December 2000

Fourthly, be very careful with shorting. An old friend used to say shorting is 10x harder than going long, even in a bear market. We recommend the vast majority of you don’t think about it. For those are undeterred, trade very small and know that you can get tire tracks on you in short squeezes. But shorting done right, as in our John Templeton example, can make exceptional profits in an environment like this.

Finally, check the market less often. The markets in a fast correction can introduce stomach churning news. Prices can move on news up down 1% in the index in the blink of an eye. If you’ve moved to safety, you don’t have to worry so much about these fluctuations and shouldn’t.